Revista IECOS, 27(1), 4-22 | Enero-Junio 2026 | ISSN 2961-2845 | e-ISSN 2788-7480

DYNAMIC RELATIONSHIP BETWEEN FINANCIAL DEVELOPMENT AND ECONOMIC GROWTH IN ASIAN ECONOMIES: A GMM ANALYSIS

RELACIÓN DINÁMICA ENTRE EL DESARROLLO FINANCIERO Y EL CRECIMIENTO ECONÓMICO EN LAS ECONOMÍAS ASIÁTICAS: UN ANÁLISIS GMM

Diba Rani Saha![]() 1, Muhammad

Rabiul Islam Liton

1, Muhammad

Rabiul Islam Liton![]() 1*, Ashiqur Rahman

1*, Ashiqur Rahman![]() 1**

1**

1 Mawlana Bhashani Science and Technology University, Dhaka, Bangladesh

E-mail: 1dibasaronika@gmail.com, 1*rabiul388@gmail.com, 1**ashiqur005@mbstu.ac.bd

1https://orcid.org/0009-0004-9220-9051, 1*https://orcid.org/0000-0002-6132-4602, 1**https://orcid.org/0009-0003-9583-1244

https://doi.org/10.21754/iecos.v27i1.2781

Recibido (Received): 27/09/2025 Aceptado (Accepted): 13/02/2026 Publicado (Published): 31/03/2026

ABSTRACT

Strong financial systems that increase productivity, promote innovation, and allow resources to be reallocated efficiently across different sectors underpin sustained economic growth in countries at various stages of development. In fact, a vibrant financial sector supports innovation, economic stability, and resilience to financial shocks. However, this is not the case for all countries. While financial institutions in developed countries tend to adjust quickly to new circumstances, those in developing countries often lack the strength to overcome hurdles to sound financial systems. Therefore, it is acknowledged that financial institutions play a major role in economic growth. This paper investigates the role of financial institutions in economic growth by analyzing the data of 27 Asian countries from 2002 to 2021. In order to do so, the paper employs a two-step System GMM estimation methodology. The paper finds that the impact of these variables differs across countries. For instance, variables like asset profitability, liquidity depth, and market trading activity are found to be positively and significantly related to growth in GDP per capita. Besides, lending to the private sector is found to be negatively related to growth, which may indicate inefficiencies in how credit is allocated in some countries. Hence, the paper concludes that since enhancements in the performance of financial systems and liquidity of equity markets support economic growth, it would be prudent for policymakers to make the strengthening of financial frameworks their top priority if they want to attain sustainable development over the long term.

Keywords: Financial Development; Banking Sector; Stock Market; Economic Growth; Two-step System GMM.

RESUMEN

Los sistemas financieros sólidos que aumentan la productividad, promueven la innovación y permiten la reasignación eficiente de los recursos entre los diferentes sectores sustentan el crecimiento económico sostenido en países que se encuentran en diversas etapas de desarrollo. De hecho, un sector financiero dinámico respalda la innovación, la estabilidad económica y la resiliencia ante las crisis financieras. Sin embargo, este no es el caso de todos los países. Mientras que las instituciones financieras de los países desarrollados tienden a adaptarse rápidamente a las nuevas circunstancias, las de los países en desarrollo a menudo carecen de la fortaleza necesaria para superar los obstáculos que impiden el establecimiento de sistemas financieros sólidos. Por lo tanto, se reconoce que las instituciones financieras desempeñan un papel importante en el crecimiento económico. En este documento se investiga el papel de las instituciones financieras en el crecimiento económico mediante el análisis de los datos de 27 países asiáticos entre 2002 y 2021. Para ello, se emplea una metodología de estimación del sistema GMM en dos etapas. El documento concluye que el impacto de estas variables difiere entre los distintos países. Por ejemplo, se ha observado que variables como la rentabilidad de los activos, la profundidad de la liquidez y la actividad comercial del mercado están relacionadas de forma positiva y significativa con el crecimiento del PIB per cápita. Además, se ha observado que los préstamos al sector privado están relacionados de forma negativa con el crecimiento, lo que puede indicar ineficiencias en la forma en que se asigna el crédito en algunos países. Por lo tanto, el documento concluye que, dado que las mejoras en el rendimiento de los sistemas financieros y la liquidez de los mercados de valores favorecen el crecimiento económico, sería prudente que los responsables políticos dieran prioridad al fortalecimiento de los marcos financieros si desean alcanzar un desarrollo sostenible a largo plazo.

Palabras clave: Desarrollo financiero; Sector bancario; Mercado bursátil; Crecimiento económico; Sistema GMM de dos pasos.

1. INTRODUCTION

Guru and Yadav (2019) emphasize that a perspective regarding development systems entails not only making the systems more efficient and stable, but also more inclusive and ultimately capable of supporting economic activities on a larger scale. Changes in the financial sectors world-wide have, during the last few decades, led to prosperity increase by making the process of forming capital easier and by being one of the main factors that help technological development. The countries whose financial systems are more advanced are likely to have a higher level as well as a more sustained rate at which an economy expands over time. Besides, giving more people the possibility to get a financial service contributes to those who are economically weaker to have a better way of dealing with economic risks and, at the same time, it helps them to invest and be more productive, which results in a decrease in poverty and in the inequality of income. Simply, a good financial system both facilitates the proper allocation of resources and provides better information regarding the investment opportunities with the highest returns.

How enhancements in banking and capital systems contribute to overall production growth has been a key topic of research for quite some time. Joseph Schumpeter's (1934) pioneering work highlighted the pivotal function of banking and capital institutions in fostering development over a long period. Later on, studies like Gurley and Shaw (1955) not only discussed that banking and capital systems should be closely linked to production performance, but they also presented production activity as a concrete output. This perspective has been backed by other scholars, such as Goldsmith (1969), McKinnon (1973), and Shaw (1973).

In fact, together, they present extensive empirical findings demonstrating the role of improved banking and capital systems in raising overall production levels. Later, in the 1990s, different growth models, including those by Greenwood and Jovanovic (1990), theorize that efficient capital systems contribute to higher overall output by reducing transaction costs and boosting productivity. Saint Paul's (1992) work goes a long way in pointing out importance of intermediaries in economic growth during innovation, specialization, and risk-sharing. At the same time, Pagano (1993) sees enhancement of banking and capital systems as one way of driving production expansion by raising the availability of available funds and their effective allocation. So, financial progress means developing well-functioning, easily accessible markets and institutions that operate under the rule of law (King & Levine, 1993). Therefore, a vibrant financial industry is the source of innovation, economic stability, and the capacity to withstand financial shocks (Guru & Yadav, 2019; Pradhan et al., 2014).

Varying institutional frameworks, policy settings, and levels of market development in Asian countries provide a complex setting for exploring dynamic relationships within their economies. Some papers focus on the part that increased credit supply and good financial intermediation play in raising output levels overall, while other papers indicate that the effect depends on other factors such as good governance, skill and education development, as well as the strength of institutions. Some Asian countries, such as Japan and Singapore, have advanced financial systems that foster growth, whereas countries in South and Southeast Asia still experience difficulties in obtaining financial inclusivity and efficiency. Because financial systems, especially banking development and stock market expansion have different effects on economic outcomes in these economies, a detailed and context- sensitive examination is essential. Hence, this paper examines how improvements in the system and market indicators relate to overall development in Asian countries by applying dynamic panel methods.

2. LITERATURE REVIEW

Many studies have explored the intricate link connecting the progress of monetary and capital systems with overall output levels. They have produced mixed outcomes, positive, negative, and no impact—depending on the country, region, and used methodology. The review focuses on financial development indicators, econometric models, and country-specific analyses. Studies, such as those by King and Levine (1993) and Beck et al. (2000), find a robust positive relationship, emphasizing banking systems' role in improving resource allocation and productivity growth. Notable some studies highlight both positive and negative impacts of financial development. Mlambo et al. (2016) found positive effects in the SADC region and OECD countries, respectively, while Adusei (2013) and Alimi (2015) observed negative relationships in Ghana and Sub-Saharan Africa and Caporale et al. (2015) found no significant impact. Some studies examine the variations in causality (unidirectional, bidirectional) and significance reflect regional.

Some research, however, conducted on banking sector (Goldsmith, 1969; King & Levine, 1993) consistently link financial intermediary efficiency to economic growth, though some exposes exceptions (Ayadi et al., 2015). Likewise, the expansion of stock trading activities has been connected to overall economic progress (Ngare et al., 2014; Bayar, 2014). The interaction of banking institutions with the equity sector, however, shows complementary roles in studies by Odhiambo (2010). However, a few study conducted on Asian context by using GMM approach. Consequently, due to inconsistent findings in previous studies, this research focuses on exploring the existing relationship of the banking sector with overall national growth.

Theoretical Perspectives on Finance and Economic Expansion

The foundation of the connection between economic growth and finance was established by Schumpeter (1911) and some followers. These scholars argue that rapid national growth requires the development of financial systems. After Schumpeter (1911) established the conceptual framework for understanding the link connecting the progress of financial structures and overall growth, economists such as McKinnon (1973), Shaw (1973), Galbis (1977), Hamilton (1790) and Pagano (1993) made significant contributions in developing the relationship. Schumpeter (1911) and his followers emphasize the role of intermediaries in supplying credit to businesses, noting that this support can trigger additional investment activities and innovations that ultimately expand the flow of goods, services, and capital. Goldsmith (1969), however, highlights the role of system growth in capital accumulation for advancing progress.

Moreover, opening up markets is regarded as a key factor in improving the efficiency of resource distribution and promoting overall expansion. The McKinnon-Shaw hypothesis (1973) argues that financial liberalization channels savings into investments, thereby fostering economic growth. In this framework, countries with limited savings can access global capital, allowing investors to diversify risks (Mollaahmetoğlu and Toprak, 2017). Despite the positive outlook of financial liberalization, there are critiques, particularly from the new structuralist school, critics argue that financial liberalization may lead to high interest rates, which do not always result in increased savings and may even cause stagflation. Notable examples include financial crises in Latin America, Mexico, and Southeast Asia, which revealed the limitations of liberalization. These crises demonstrate that, although financial markets expanded, they do not necessarily support the real sector, thereby exacerbating long-term economic issues (Has, 2007; Akyüz, 1993).

Theoretical Approaches to the Interaction between Finance and Economic Expansion

The relationship linking the progress of monetary and capital systems with overall output expansion is widely debated over a long period. Several theoretical frameworks explore the link connecting monetary and capital system progress with output expansion, highlighting different directions of causality.

Supply-Leading Hypothesis: Aligning with neo-classical economic theory, the supply-leading hypothesis proposes that a liberalized monetary and capital system markets encourage savings and direct them to high-productivity areas and hence leading to economic growth. Scholars like Bagehot (1873), Schumpeter (1912) and McKinnon (1973) support this view, which has been reinforced by empirical studies (Goldsmith, 1969; King & Levine, 1993; Levine, 1997). However, in recent research, conducted by Yağlı and Topçu (2019) and Ergur and Özek (2020), indicates supply-side influences over time, demonstrating that the expansion of capital and monetary markets fosters output expansion by enhancing labor productivity and overall system efficiency.

Demand-Following Hypothesis: The other side of the argument says that most of the improvement in the monetary and capital systems is a response to aggregate economic growth. As the average income of a person increases, the demand for money and capital services also rises, and this is what drives the growth of the financial system. This line of thought which is derived from the work of Robinson (1952) and Patrick (1966), maintains that alongside the growth of production activities, the requirement for more advanced monetary and capital services and tools also increases, a connection that has been proven by various studies conducted by Jung (1986), Gurley and Shaw (1973), and Zengin (2023).

The demand-following argument is in accordance with the objections against financial liberalization, especially from new structuralist and Keynesian viewpoints. Critics argue that liberalization does not necessarily produce higher levels of resource accumulation and may instead create distortions and instability in developing countries (Cicioğlu, 2009).

They further highlight the stagflationary risks of financial liberalization that we have observed in various financial crises and they question the assumption of the unqualified benefits of financial market liberalization for economic growth.

Bidirectional Hypothesis: The bidirectional hypothesis suggests a mutual association between finance and expansion, in which advancements in monetary and capital systems and overall output mutually support their progress. Growth theories of this approach support the idea by indicating that progress in monetary and capital systems improves the efficiency of resource allocation, fostering capital accumulation and fosters overall output expansion (Greenwood and Jovanovic, 1990). Thus, this reciprocal relationship indicates that output expansion and progress in monetary and capital systems are closely linked, fostering a process that reinforces one another.

Bidirectional Hypothesis: The bidirectional hypothesis proposes that finance and expansion are mutually related, so that each development in the monetary and capital systems and overall output serves as a support to the progress of the other. Growth models of this approach are in support of the notion by pointing out that development in monetary and capital systems not only enhances the ease of resource use but also capital accumulation and production growth are typical consequences of it (Greenwood and Jovanovic, 1990). Hence, this two-way relationship suggests that production growth and the development of monetary and capital systems are extremely interdependent, nurturing a process that keeps one another going.

3. METHODOLOGY

Description of the Data and Variable’s Sources

This investigation relies on an unbalanced panel dataset that contains 540 observations for 27 Asian economies spanning the years 2002 to 2021. The database compiles information on the expansion of the financial system, per capita GDP growth, and several additional control factors. Most of the statistics were obtained from the World Bank’s World DataBank, except for the variables related to the performance of the financial sector. These particular indicators were sourced from the World Bank’s Global Financial Development database. A concise overview of the variables is provided below:

Table1

Overview of the Variables and Their Data Origins

|

Variables |

Symbol |

Definition |

Expected Sign |

Source |

|

GDP Per Capita Growth |

GROWTH |

Growth rate of GDP per capita |

+ |

WDI |

|

Liquid Liabilities |

LIQ.LIAB |

Liquid liabilities (% of GDP) |

+ |

WDI |

|

Credit to Private Sector |

DCPS |

Domestic credit to private sector (% of GDP) |

+ |

WDI |

|

Return of Assets |

ROA |

Bank return on assets (%, before tax) |

+ |

WDI |

|

Turnover Ratio |

TOR |

Stock market turnover ratio (% of GDP) |

+ |

WDI, |

|

Trade |

TRD |

Trade (% of GDP) |

+ |

WDI |

|

Inflation Rate |

INFL |

Inflation, consumer prices (annual %)

|

- |

WDI |

|

Government Expenditure |

GOVC |

General government final consumption expenditure (% of GDP) |

+/- |

WDI |

|

Physical Investment |

GFCF |

Gross fixed capital formation (% of GDP) |

+ |

WDI |

|

Population Growth |

POP |

Population growth (annual %) |

+ |

WDI |

Estimation Technique

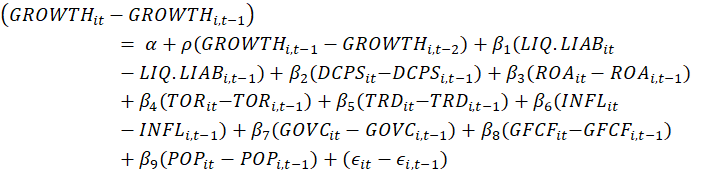

Given its methodological benefits compared with purely cross-sectional or time-series approaches particularly its ability to account for unobserved factors that remain constant over time the analysis adopts a panel data framework. This structure enhances the precision and reliability of the estimated coefficients results by increasing degrees of freedom, variability, and information content while decreasing co-linearity and the likelihood of omitted variable bias. Nevertheless, the panel data has additional issues with heteroscedasticity, autocorrelation, and endogeneity. However, presence of endogeneity and heteroscedasticity it can be mitigated by applying the GMM approach. Hence, the study employed two-steps system GMM in its analysis. The procedure introduced by Arellano and Bond (1991) is employed to detect the presence of serial correlation in the error terms. In addition, the validity of the selected instruments is assessed through the test proposed by Lars Peter Hansen, which examines the consistency of the model’s overidentifying restrictions.

A general dynamic panel regression model is given below:

![]()

In

this specification, Y denotes the outcome variable, while X represents a set of

explanatory factors. The term ![]() captures unobserved,

country-specific effects that remain constant over time, and 𝜀 corresponds to the

random error component, assumed to follow a normal distribution. (0,

captures unobserved,

country-specific effects that remain constant over time, and 𝜀 corresponds to the

random error component, assumed to follow a normal distribution. (0,![]() ); "i" and "t" indicate country

and time, respectively.

); "i" and "t" indicate country

and time, respectively.

Specification of used dynamic version can be expressed as follows:

where

dependent variable ![]() the dependent variable reflects per capita GDP growth, widely

regarded as a robust proxy for overall economic performance (Andersen et al.,

2003; Arellano & Bond, 1991).

the dependent variable reflects per capita GDP growth, widely

regarded as a robust proxy for overall economic performance (Andersen et al.,

2003; Arellano & Bond, 1991).

The level of financial sector advancement is captured through four key measures: LIQ.LIAB (ratio of liquid liabilities to GDP), DCPS (credit allocated to the private sector relative to GDP), ROA (return on assets), and TOR (stock market turnover ratio).

The

vector Xit comprises additional explanatory factors, including TRD (trade

openness), INFL (inflation rate), GOVC (general government final consumption

expenditure), GFCF (gross fixed capital formation as a share of GDP), and POP

(population growth), which are incorporated as control variables. The

disturbance component is denoted by ![]() , while β represents the set of coefficients to

be estimated.

, while β represents the set of coefficients to

be estimated.

To examine the influence of financial sector advancement on per capita GDP growth, the baseline empirical specification is formulated as follows:

However, two tests is conducted for the model using the GMM estimator. The validity of the selected instruments is evaluated through the Sargan test of overidentifying restrictions, following established practices in prior studies employing the GMM (Kumar and Bird 2020; Arellano and Bond, 1991; Klein and Weill 2022; Beck and Levine, 2004; Roodman, 2009).

4. RESULT ANALYSIS AND DISCUSSION

Descriptive Statistics and Correlation Analysis

Table 5.1 presents a detailed overview of the descriptive measures for each variable, reporting the total number of observations, the average value, the measure of dispersion, as well as the corresponding minimum and maximum figures.

Variability in each distribution is reflected by standard deviation. The following standard deviations are recorded: liquid liabilities (73.99%), credit allocated to private sector within domestic economy (47.57%), trade (84.92%), government expenditure (4.93%), and physical capital (6.64%). These figures indicate that the data are relatively dispersed around their central values, with the standard deviations being lower than the mean in most cases. In contrast, dispersion measure for income growth per person, return on assets, turnover ratio, inflation rate, and population growth are 4.51%, 2.81%, 65.47%, 8.60% and 2.52% respectively. These are larger than their corresponding mean values, suggesting greater variability in these economic indicators over time.

Table 2

Descriptive Statistics

|

Variables |

Observation |

Mean |

Std. Deviation |

Min |

Max |

|

GROWTH |

540 |

2.87385 |

4.50882 |

-20.129 |

19.0059 |

|

LIQ.LIAB |

525 |

93.7517 |

73.9969 |

11.6714 |

454.65 |

|

DCPS |

445 |

77.0366 |

47.5694 |

14.6822 |

258.949 |

|

ROA |

539 |

1.54997 |

2.8137 |

-55.412 |

21.9248 |

|

TOR |

509 |

57.0773 |

65.4682 |

0.04 |

480.287 |

|

TRD |

535 |

100.559 |

84.9206 |

20.4471 |

442.62 |

|

INFL |

534 |

4.78841 |

8.60441 |

-4.8633 |

154.756 |

|

GOVC |

540 |

13.9039 |

4.93117 |

2.36014 |

30.1779 |

|

GFCF |

539 |

25.6132 |

6.63587 |

5.35948 |

48.8691 |

|

POP |

540 |

1.62744 |

2.52403 |

-10.927 |

21.7003 |

|

Source: The author's calculations using the STATA 2014 software. |

|||||

Unconditional Cross-Correlations Analysis

The unconditional cross-correlation results reported in Table 3 indicate that real income growth per person is positively associated with investment in fixed assets relative to GDP. In contrast, it is negatively correlated with inflation, trade (% of GDP), demographic expansion and public sector final consumption spending (% of GDP). In relation to the central research objective, the findings indicate that real income growth per person is inversely associated with credit extended to the private sector and overall liquidity in the economy, whereas it exhibits a positive relationship with profitability measured by return on assets and with the stock market trading activity reflected in the turnover ratio.

Correlation Matrix

|

Variables |

GROWTH |

LIQ. LIAB |

DCPS |

ROA |

TOR |

TRD |

INFL |

GOVC |

GFCF |

POP |

|

GROWTH |

1 |

|

|

|

|

|

|

|

|

|

|

LIQ.LIAB |

-0.103* |

1 |

|

|

|

|

|

|

|

|

|

DCPS |

-0.069 |

0.839* |

1 |

|

|

|

|

|

|

|

|

ROA |

0.133* |

-0.122* |

-0.389* |

1 |

|

|

|

|

|

|

|

TOR |

0.094* |

0.154* |

0.309* |

-0.038 |

1 |

|

|

|

|

|

|

TRD |

-0.019 |

0.514* |

0.488* |

-0.017 |

-0.119* |

1 |

|

|

|

|

|

INFL |

-0.084 |

-0.346* |

-0.426* |

-0.009 |

0.003 |

-0.125* |

1 |

|

|

|

|

GOVC |

-0.271* |

0.069 |

0.109* |

-0.059 |

0.15* |

-0.199* |

-0.24* |

1 |

|

|

|

GFCF |

0.229* |

0.043 |

0.173* |

0.02 |

0.228* |

-0.104* |

-0.15* |

-0.03 |

1 |

|

|

POP |

-0.397* |

-0.107* |

-0.212* |

0.049 |

-0.07 |

0.039 |

-0.017 |

0.071 |

0.064 |

1 |

|

Note: The symbol “*” denotes significance at the 5%, level. |

||||||||||

Two Step System GMM Results Analysis

The outcomes derived from the dynamic panel estimation approach are displayed in Table 4.

Table 4

Results of the dynamic panel modeling procedure

|

Outcome Measure: Growth in income per person |

||||

|

Explanatory Variables |

Coefficients |

Corrected Std. Err. |

t |

P>|t| |

|

L.GROWTH |

.3438628*** |

.0711244 |

4.83 |

0.000 |

|

LIQ.LIAB |

.0074212* |

.0043165 |

1.72 |

0.097 |

|

DCPS |

-.0239551*** |

.0082688 |

-2.90 |

0.008 |

|

ROA |

.5213341** |

.2251157 |

2.32 |

0.029 |

|

TOR |

.0055804** |

.0023271 |

2.40 |

0.024 |

|

TRD |

.0046074** |

.0020006 |

2.30 |

0.030 |

|

INFL |

.0034547 |

.0633153 |

0.05 |

0.957 |

|

GOVC |

-.0728419 |

.0559014 |

-1.30 |

0.204 |

|

GFCF |

.0908458* |

.0528523 |

1.72 |

0.098 |

|

POP |

-.5665823*** |

.0738816 |

-7.67 |

0.000 |

|

Constant |

.7134382 |

1.288135 |

0.55 |

0.584 |

|

N=397, Group=27, F test: Prob > F = 0.000, A-B test (1st) AR (1): z = -3.05, Prob > z = 0.002, A-B test (2nd) AR (2): z = -1.05, Prob > z = 0.293, Sargan Test: chi2(17) = 37.09, Prob > chi2 = 0.003, Hansen test: chi2(17) = 22.74 , Prob > chi2 = 0.158 |

||||

Note: The symbols *, **, and *** denote the significance levels of 10%, 5%, and 1%, respectively.

Findings obtained from the system GMM estimation approach reveal that most variables—namely L.GROWTH, LIQ.LIAB, TOR, TRD, GFCF, and ROA—exert a positive influence on overall economic performance. In contrast, DCPS and POP display an adverse relationship with overall economic performance. The estimated coefficient for L.GROWTH (0.3439) indicates that previous income growth per person exerts a statistically significant and positive influence on its current level. Specifically, a 1% rise in the lagged growth rate is linked to an approximate 0.344% increase in present income growth per person, holding other determinants constant. The estimated parameter for LIQ.LIAB (0.0074212) indicates a positive association with the outcome variable. By contrast, the coefficient on DCPS suggests that a higher volume of financing extended to private economic agents may be related to a slower rate of income growth per person. Findings indicate that a 1% rise in financing directed to private economic agents is associated with an approximate 0.024% decline in income per person. Comparable evidence is reported by Cournède et al. (2015). In addition, return on assets demonstrates a direct relationship with overall macroeconomic performance. Other influential factors holding same 1% increase of returns on assets in the Asian countries may increases GDP growth by 0.52 %. The economic impact of banks becoming more profitable is positive, as evidenced by the fact that for every 1% increase in return on assets (ROA), GDP per capita rises by 0.52%. This relationship suggests that more profitable banks, with greater capital on hand, have stronger incentives to effectively screen and monitor loans. Consequently, firms become more capable of mobilizing funds efficiently within the productive system. Moreover, the turnover ratio (TOR), which reflects the intensity of trading activity in the stock market, proves to be significant in the estimated models. The direction and relevance of the turnover coefficient are consistent with the evidence reported (Beck et al., 2004). Evidence indicates that a higher level of trading activity in equity markets is associated with an expansion in output per person. Specifically, a 1% rise in this trading intensity measure corresponds to an approximate 0.006% increase in output. These results are consistent with the conclusions reached by Beck et al. (2004), as well as by Valickova et al. (2015).

This analysis indicates that trade openness is directly associated with improvements in overall macroeconomic performance. An 1% increase in trade may increase GDP growth by 0.005 % if other factors remain unchanged. Similar result was found in Breusch& Pagan (1980) albeit Baltagi et al. (2009) detect an adverse effect. This analysis shows that trade openness is directly associated with overall macroeconomic performance, and this relationship is supported by statistical evidence. An increase of 1% trade may increase GDP growth by 0.005 % in the Asian countries. Government expenditure (GOVC) has been found to be statistically insignificant in the regression; however, its effect contradicts the expected sign. A 1% rise in public sector spending ratio may resulted in 0.728 % decline in GDP. The inverse link suggests that increased government spending will likely result in lower Income expansion per person. This divergence can be interpreted through a Keynesian perspective, which posits that government spending supports sustained expansion in overall output. When evaluating the immediate effects of public expenditure, it can be inferred that it does not stimulate output in the short term, since the variables capture direct and contemporaneous impacts. Capital accumulation is a key driver of immediate productive activity as well as future expansion capacity, thereby exerting a direct influence on overall output. For the group of nations examined, the estimated parameter associated with investment is 0.091, and it reaches conventional levels of statistical relevance, with a p-value of 0.098. This direct coefficient implies that a one-unit rise in investment results in a 0.091 increase in income expansion per person, suggesting that greater levels of capital allocation are linked to higher output per individual. Within this specification, the inflation rate does not exhibit a meaningful association with overall macroeconomic performance across the Asian economies examined. The negative coefficient of -0.5666 for population growth (POP) suggests an inverse relationship as the number of people increases and earnings per person decline. This result shows a strong and statistically meaningful effect (p = 0.000) shows that rapid population expansion slows the expansion of GDP per individual, most likely due to increased resource consumption and consequent capital dispersion.

5. CONCLUSIONS

Advancement in the banking and capital system serves as a key driver of the economic process, helping to maintain a stable link between improvements in the monetary system and overall output expansion. Findings from the panel analysis indicate that variables representing banking and capital system progress, measured through liquid liabilities, Return on Assets (ROA), and trading activity intensity also show a notable direct effect on output expansion in Asian countries, whereas the measure of domestic financing extended to private economic agents exhibits a negative influence on overall performance. Therefore, the results of this study provide credibility to the beliefs (Schumpeter et al., 1934; McKinnon, 1973; Shaw, 1973) that financial development is a major force behind economic expansion. Thus this research suggests the policymakers to enhance financial infrastructure for promoting sustainable economic growth. To do these-

§ Efforts should be directed toward enhancing the operational effectiveness of banking and capital institutions such as adopting advanced risk management practices, promoting transparency, and enhancing efficiencies in credit allocation.

§ Authorities should ensure financing provided to private economic agents is allocated toward productive activities. Incentives should be implemented to motivate banks to invest in important sectors that present significant growth prospects.

- Asian countries should focus on improving capital markets for easier loans for SMEs to access stock exchanges, helping to boost the economy’s growth and productivity.

AUTHORS CONTRIBUTION STATEMENT

Diba Rani Saha: Conceptualization, Investigation, Methodology, Writing – original draft, Writing – review & editing.

Ashiqur Rahman: Formal analysis, Visualization, Writing – review & editing.

Muhammad Rabiul Islam Liton: Validation, Writing – review & editing

REFERENCES

Adusei, M. (2013). Financial development and economic growth: Evidence from Ghana. The International Journal of Business and Finance Research, 7(5), 61-76.

https://www.academia.edu/download/84671821/IJBFR-V7N5-2013-6.pdf

Akyüz, Y. (1993). Financial liberalization: the key issues (No. 56). UNCTAD.

https://www.southcentre.int/wp-content/uploads/2013/08/REP1_FInancial-Liberalization_EN.pdf

Alimi, R. S. (2015). Financial deepening and economic growth: A System GMM Panel Analysis with application to 7 SSA countries. MPRA.

https://mpra.ub.uni-muenchen.de/id/eprint/65789

Andersen, T. B., & Tarp, F. (2003). Financial liberalization, financial development and economic growth in LDCs. Journal of International Development: The Journal of the Development Studies Association, 15(2), 189-209.

https://doi.org/10.1002/jid.971

Arellano, M., and Bond, S. (1991). Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. The review of economic studies, 58(2), 277-297. https://doi.org/10.2307/2297968

Ayadi, R., Arbak, E., Naceur, S. B., & De Groen, W. P. (2015). Financial development, bank efficiency, and economic growth across the Mediterranean (pp. 219-233). Springer International Publishing. https://doi.org/10.1007/978-3-319-11122-3_14

Bagehot, W. (1873). Lombard Street: A description of the money market. The North American Review, 119(245), 331-358. https://www.jstor.org/stable/25109861

Baltagi, B. H., Demetriades, P. O., & Law, S. H. (2009). Financial development and openness: Evidence from panel data. Journal of development economics, 89(2), 285-296. https://doi.org/10.1016/j.jdeveco.2008.06.006

Bayar, Y. (2014). Financial development and economic growth in emerging Asian countries. Asian Social Science, 10(9), 8. https://doi.org/10.5539/ass.v10n9p8

Beck, T., & Levine, R. (2004). Stock markets, banks, and growth: Panel evidence. Journal of Banking & Finance, 28(3), 423-442.

https://doi.org/10.1016/S0378-4266(02)00408-9

Beck, T., Levine, R., & Loayza, N. (2000). Finance and the Sources of Growth. Journal of financial economics, 58(1-2), 261-300.

https://doi.org/10.1016/S0304-405X(00)00072-6

Breusch, T. S., & Pagan, A. R. (1980). The Lagrange multiplier test and its applications to model specification in econometrics. The review of economic studies, 47(1), 239-253. https://doi.org/10.2307/2297111

Caporale, G. M., Rault, C., Sova, A. D., & Sova, R. (2015). Financial development and economic growth: Evidence from 10 new European Union members. International Journal of Finance & Economics, 20(1), 48-60.

https://doi.org/10.1002/ijfe.1498

Cicioğlu, S. (2009). Financial Depth and Dominance Analysis in The Turkish Economy in The Process of Financial Liberalization (Doctoral Dissertation). Marmara University, Institute of Social Sciences, Istanbul, Turkey.

Cournède, B. and Denk, O. (2015). Finance and economic growth in OECD and G20 countries. OECD Economics Department Working Papers, No. 1223, OECD Publishing, Paris. https://dx.doi.org/10.2139/ssrn.2649935

Ergür, H., & Özek, Y. (2020). Brıcs-T Ülkelerinde Finansal Gelişmenin Ekonomik Büyümeye Etkisi. Kahramanmaraş Sütçü İmam Üniversitesi Sosyal Bilimler Dergisi, 17(1), 343-357. https://doi.org/10.33437/ksusbd.690132

Galbis, V. (1977). Financial intermediation and economic growth in less‐developed countries: A theoretical approach. The Journal of Development Studies, 13(2), 58–72. https://doi.org/10.1080/00220387708421622

Goldsmith, R. W. (1969). Financial structure and development. Yale University.

https://cir.nii.ac.jp/crid/1971149384850352262/holdings

Greenwood, J., & Jovanovic, B. (1990). Financial development, growth, and the distribution of income. Journal of political Economy, 98(5, Part 1), 1076-1107.

https://doi.org/10.1086/261720

Gurley, J. G., & Shaw, E. S. (1955). Financial aspects of economic development. The American economic review, 45(4), 515-538.

https://www.jstor.org/stable/1811632

Guru, B. K., & Yadav, I. S. (2019). Financial development and economic growth: panel evidence from BRICS. Journal of Economics, Finance and Administrative Science, 24(47), 113-126. https://doi.org/10.1108/JEFAS-12-2017-0125

Hamilton, A. (1790). Report on the Public Credit. United States Department of the Treasury.

https://oll.libertyfund.org/pages/1790-hamilton-first-report-on-public-credit

Has, H. (2007). Control of Speculative Capital Movements and Policy Recommendations for Turkey. Capital Markets Board Auditing Department Qualification Study, Istanbul.

Jung, W. S. (1986). Financial development and economic growth: international evidence. Economic Development and cultural change, 34(2), 333-346.

https://doi.org/10.1086/451531

King, R. G., & Levine, R. (1993). Finance, entrepreneurship and growth. Journal of Monetary economics, 32(3), 513-542.

https://doi.org/10.1016/0304-3932(93)90028-E

Klein, P. O., & Weill, L. (2022). Bank profitability and economic growth. The Quarterly Review of Economics and Finance, 84, 183-199.

https://doi.org/10.1016/j.qref.2022.01.009

Kumar, V., & Bird, R. (2020). Do profitable banks make a positive contribution to the economy?. Journal of Risk and Financial Management, 13(8), 159.

https://doi.org/10.3390/jrfm13080159

Levine, R. (1997). Financial development and economic growth: views and agenda. Journal of economic literature, 35(2), 688-726.

https://www.jstor.org/stable/2729790

McKinnon, R. (1973). Money and Capital in Economic Development. The Brooking Institute, Washington DC. https://n9.cl/2u05e4

Mlambo, C., Kushamba, A., &Simawu, M. B. (2016). China-Africa relations: What lies beneath? The Chinese Economy, 49(4), 257-276.

https://doi.org/10.1080/10971475.2016.1179023

Mollaahmetoğlu, E., & Topak, M. S. (2017). The impact of global capital flows on firms’ performance: evidence from Turkey. İstanbul Gelişim Üniversitesi Sosyal Bilimler Dergisi, 4(2 (ICEFM 2017 Özel Sayısı/Special Issue of ICEFM 2017)), 1-16. https://dergipark.org.tr/en/download/article-file/417266

Ngare, E., Nyamongo, E. M., &Misati, R. N. (2014). Stock market development and economic growth in Africa. Journal of Economics and business, 74, 24-39.

https://doi.org/10.1016/j.jeconbus.2014.03.002

Odhiambo, N. M. (2010). Are banks and stock markets positively related? Empirical evidence from South Africa. Journal of Applied Business Research (JABR), 26(6).

https://www.proquest.com/openview/19993965b67dbcd1ff581a1f6d978e7e/1?pq-origsite=gscholar&cbl=30135

Pagano, M. (1993). Financial markets and growth: An overview. European economic review, 37(2-3), 613-622. https://doi.org/10.1016/0014-2921(93)90051-B

Patrick, H. T. (1966). Financial development and economic growth in underdeveloped countries. Economic development and Cultural change, 14(2), 174-189.

https://doi.org/10.1086/450153

Pradhan, R. P., Arvin, M. B., Hall, J. H., & Bahmani, S. (2014). Causal nexus between economic growth, banking sector development, stock market development, and other macroeconomic variables: The case of ASEAN countries. Review of Financial Economics, 23(4), 155-173. https://doi.org/10.1016/j.rfe.2014.07.002

Robinson, J. (1952). The civilizations of the general theory. The Rate of Interest and Other Essays.

Roodman, D. (2009). How to do xtabond2: An introduction to difference and system GMM in Stata. The stata journal, 9(1), 86-136.

https://doi.org/10.1177/1536867X0900900106

Saint, P. G. (1992). Technological choice, financial markets and economic development. European Economic Review, 36(4), 763-781.

https://doi.org/10.1016/0014-2921(92)90056-3

Schumpeter, J. A. (1911). The Theory of Economic Development. An Inquiry into Profits, Capital, Credit, Interest, and the Business Cycle. Cambridge, MA: Harvard University Press.

Schumpeter, J. A. (1912). The theory of economic development: An inquiry into profits, capital, credit, interest, and the business cycle. Duncker & Humblot.

Schumpeter, J. A., & Opie, R. (1934). The theory of economic development: an inquiry into profits, capital, credit, interest, and the business cycle. Harvard University Press.

https://cruel.org/books/hy/shortschumpeter/SchumpeterTheoryofEconDev.pdf

Shaw, E.S. (1973) Financial Deepening in Economic Development. Oxford University Press. https://n9.cl/vibe3

Valickova, P., Havranek, T., & Horvath, R. (2015). Financial development and economic growth: A meta‐analysis. Journal of economic surveys, 29(3), 506-526.

https://doi.org/10.1111/joes.12068

Yağlı, İ., & Topcu, E. (2019). Finansal gelişme ve ekonomik büyüme arasındaki nedensellik ilişkisi: G7 ülkeleri örneği. Afyon Kocatepe Üniversitesi Sosyal Bilimler Dergisi, 21(3), 888-898. https://doi.org/10.32709/akusosbil.523505

Zengin, B. (2023). Finansal Gelişmenin Ekonomik Büyümeye Etkisi: Türkiye Ekonomisinin Toda-Yamamoto Yaklaşımıyla Analizi. İşletme Araştırmaları Dergisi, 15(3), 2331-2346.

https://www.ceeol.com/search/article-detail?id=1203876