Revista IECOS, 26(2), 70-95 | Julio-Diciembre 2025 | ISSN 2961-2845 | e-ISSN 2788-7480

PURCHASING POWER PARITY BETWEEN PERU AND CHINA: ANALYSIS OF TRADE AND INFLATION (2002-2019)

PARIDAD DEL PODER ADQUISITIVO ENTRE PERÚ Y CHINA: ANÁLISIS DEL COMERCIO Y LA INFLACIÓN (2002-2019)

Ana

Cristhel Correa Lozada![]()

Universidad Nacional de Trujillo, La Libertad, Peru

E-mail: anacristhel.cl@gmail.com

https://orcid.org/0009-0004-2265-8329

https://doi.org/10.21754/iecos.v26i2.2690

Recibido (Received): 04/07/2025 Aceptado (Accepted): 07/09/2025 Publicado (Published): 30/09/2025

ABSTRACT

This research explores the application of the Purchasing Power Parity (PPP) theory in the context of trade between Peru and China during the period 2002-2019. The PPP, developed to investigate the link between exchange rates and market prices, remains relevant in a globalized environment where economies are interconnected. Trade between the two countries has grown exponentially, highlighting the need to understand how variations in inflation rates affect the nominal exchange rate (NER). Using an Error Correction Model (VECM), this study examines the validity of the PPP theory in this trade relationship, providing valuable insights for the formulation of economic policies and foreign trade strategies. This study confirms the long-term relationship between inflation and exchange rates, which is also influenced by structural factors and global events. These include external shocks, including global financial crises, which can distort the expected inflation-exchange rate relationship. The results are useful to assess the coherence of exchange rate adjustments with differences in inflation rates, which is crucial for designing effective economic policies and promoting lasting economic stability in the context of growing global interdependence.

Keywords: purchasing power parity, relative purchasing power parity, law of one price, Peru-China trade, exchange rate dynamics, cointegration analysis.

JEL Classification: F31, C32, E31, F14, F41

RESUMEN

Esta investigación explora la aplicación de la teoría de la paridad del poder adquisitivo (PPA) en el contexto del comercio entre Perú y China durante el período 2002-2019. La PPA, desarrollada para investigar la relación entre los tipos de cambio y los precios de mercado, sigue siendo relevante en un entorno globalizado en el que las economías están interconectadas. El comercio entre ambos países ha crecido exponencialmente, lo que pone de relieve la necesidad de comprender cómo las variaciones de las tasas de inflación afectan al tipo de cambio nominal (TCN). Utilizando un modelo de corrección de errores (VECM), este estudio examina la validez de la teoría de la PPA en esta relación comercial, proporcionando información valiosa para la formulación de políticas económicas y estrategias de comercio exterior. Este estudio confirma la relación a largo plazo entre la inflación y los tipos de cambio, que también se ve influida por factores estructurales y acontecimientos mundiales. Entre ellos se incluyen las perturbaciones externas, como las crisis financieras mundiales, que pueden distorsionar la relación esperada entre la inflación y el tipo de cambio. Los resultados son útiles para evaluar la coherencia de los ajustes de los tipos de cambio con las diferencias en las tasas de inflación, lo que es crucial para diseñar políticas económicas eficaces y promover una estabilidad económica duradera en el contexto de una creciente interdependencia mundial.

Palabras clave: paridad del poder adquisitivo, paridad del poder adquisitivo relativa, ley del precio único, comercio Perú-China, dinámica del tipo de cambio, análisis de cointegración.

1 INTRODUCTION

In the current context, economies are interconnected in an unprecedented way, facilitating the exchange of large volumes of goods and services. This global economic integration has accentuated the relevance of Purchasing Power Parity (PPP) by establishing the first step to identify the implicit factors that exist in the dynamics of different countries that maintain trade relations and to know the way in which the values of goods and services are determined when compared with each other (Craig, 2005). The theory of Purchasing Power Parity is a fundamental concept in economics that examines the relationship between cross-country price levels of goods and services and the exchange rates connecting their currencies. Developed in the context of international exchange and monetary policy, the PPP was formally introduced after World War I by Cassel, who recommended the use of the PPP to determine exchange rates between countries. He observed that in the wake of World War I, nations such as Germany, Hungary, and the Soviet Union faced not only hyperinflation, but also a significance decline in the purchasing power of their currencies. Consequently, the currency experienced a notable depreciation relative to stronger currencies, particularly the U.S. dollar (Rogoff, 1996). Based on these observations, Cassel proposed a model where the hypothesis of free movement of goods and trade would lead to a convergence towards PPP among the currencies of different countries, as indicated by their domestic price levels (Salcedo Muñoz, 2020). From then onward, the theory has been used as a standard framework to evaluate and forecast long-term nominal currency values.

The case of Peru and China illustrates in an exemplary way the application of the PPP in a modern economic environment. Just a few years ago, the United States was the benchmark country for measuring or comparing productivity advances and improvements, as suggested by the work of Laurente Blanco & Machaca Hancco (2020). However, with multilateral openness and the gradual growth of trade, new markets and opportunities for exchange opened up. This is how China became one of the largest recipients of foreign capital and is now our main trading partner (Urriola et al., 2020). Over the last twenty years, the business relationship between the two countries has grown dramatically. In 2002, total trade between Peru and China was approximately 1,063 million dollars, while in 2019 this volume had multiplied by 22, reaching 23,769 million dollars (Comex Peru, 2020). This boom in trade has been driven by various factors, involving the deregulation of markets along with the implementation of the 2010 Free Trade Agreement, which facilitated a more dynamic exchange of goods and services (BCRP, 2019). Peru's growing dependence on foreign trade, with China as its main trading partner, makes it essential to investigate the macroeconomic relationships that underlie this economic interdependence.

The study of the PPP in the trade relationship between Peru and China is particularly relevant due to the distinctive characteristics of these economies. China, an emerging economy that has experienced unprecedented economic growth in recent decades, has established itself as one of the world's largest economies and a key player in global trade (H. Cordesman, 2023). Peru, on the other hand, is a developing economy that has experienced significant, albeit more modest, economic growth and is heavily dependent on its natural resource exports (Worl Bank Group, 2024). These structural differences, together with fluctuations in their respective inflation rates, make the analysis of the PPP a crucial exercise in understanding exchange rate dynamics and their impact on bilateral trade between the two countries.

Recent research explored PPP dynamics in emerging economies, confirming nonlinear adjustment patterns and factors that may skew the theory of ideal behavior in the short term. For example, She et al. (2020) conducted a study that analyses, developed, emerging, and frontier economies, drawing on information from 45 nations and employing different unit root procedures, such as the Fourier KPSS test. The results show that the PPP is valid in this type of economy, although not uniformly, highlighting how the theory tends to be partially fulfilled due to the presence of frictions in the market and institutional factors that alter the ideal theoretical adjustment. Likewise, a study on Economic Community of West African States (ECOWAS), conducted by (Nathaniel, 2019), applied unit root tests such as the Augmented Dickey-Fuller test (ADF), the Phillips-Perron test (PP) and the unit root test with breakpoint (URB), as well as panel cointegration tests. The findings revealed that, although the PPP hypothesis holds true in the short term in ECOWAS member countries, its compliance in the long term is mixed. This suggests that the validity of the PPP is not completely uniform across the region, due to differences in exchange rate regimes and structural factors that affect the ideal theoretical long-term adjustment.

Despite its relevance, the empirical use of PPP has generated significant discussion in the economic literature (M. Taylor & P. Taylor, 2004), particularly in the context of emerging economies such as Peru and China. While PPP provides a valuable framework for examining exchange rates over the long horizon, a wide body of research indicates that the theory often fails in the short run due to factors like government participation in currency markets, trade restrictions, and price rigidities in goods and services. For instance, Xie, Chen, and Hsieh (2021) found that the applicability of PPP may be influenced by structural breaks—both transitory and permanent—within the economies studied. Their findings also suggest that variables such as economic size and the debt-to-GDP ratio significantly affect whether the theory holds in the long term. Moreover, market imperfections, including transport expenses and tariff measures, can generate short-term departures from PPP.

The research will deepen knowledge on the use of PPP in contemporary international commerce and generate insights that can guide both economic policies and foreign trade approaches. As Peru and China continue to strengthen their economic ties, understanding how PPP theory manifests itself in their trade relationship is critical to designing effective policies that promote economic stability and sustainable growth.

This paper starts by presenting the research background, describing how PPP theory is applied to the bilateral economic relationship between Peru and China, with emphasis on inflation and nominal exchange rates. The following section analyzes both economies’ performance, focusing on exchange rate dynamics and inflationary developments. The third section details the econometric approach, including unit root and cointegration testing, and interprets the findings. The closing section discusses the broader implications of the results for evaluating PPP in the Peru–China trade context.

2. LITERATURE REVIEW

2.1. The theory of payment power parity

According to the Purchasing Power Parity theory, exchange rates should correspond to the relative price levels of two countries. Thus, if inflation reduces a currency’s real value, its nominal exchange rate depreciates; whereas stronger purchasing power is generally associated with appreciation (Imbz et al., 2005).

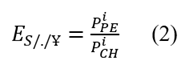

PPP stems from the Law of One Price (LOP), which maintains that under perfect competition and without tariffs, quotas, or transport costs, comparable goods should cost the same across borders when converted into a single currency. This principle is represented mathematically as:

![]()

Where ![]() is the price in PEN

of good "i" when sold in Peru,

is the price in PEN

of good "i" when sold in Peru, ![]() is NER PEN/CNY and

is NER PEN/CNY and ![]() is the price of

good "i" in Chinese yuan when sold in China.

is the price of

good "i" in Chinese yuan when sold in China.

Equivalently, the PEN/CNY exchange rate is the ratio of Peruvian and Chinese monetary prices:

Extending equation (2) to PPP theory and rearranging, we have:

![]()

Equation (3) presents on its left, the value in Peruvian soles of a basket of goods consumed domestically, and on its right, the equivalent cost of that basket in China, expressed in PEN after conversion. In other terms, the right side illustrates the real purchasing power of the Peruvian currency in the Chinese market. Thus, PPP provides a theoretical explanation of exchange rate fluctuations between two nations as a function of relative price level changes.

When comparing equation (1) with (3), we can see that the difference between the single price law and the PPP is that the LPU addresses individual items (such as product i), while the PPP is a broader concept that refers to a basket of commodities and is applied at the general price level. If the LPU is valid for each product, then the PPP should be automatically maintained provided that the reference baskets used to calculate the price indices of different countries are identical.

Even when the single price law is not enforced for every individual product, the argument holds that prices and exchange rates should not deviate substantially from the PPP. If goods and services temporarily become more expensive in one country compared to another, demand for those products and currencies diminishes. Through this mechanism, domestic prices and the exchange rate are realigned with the level implied by PPP. Conversely, the opposite conditions generate appreciation of the currency and rising inflation. The key premise of PPP is therefore that, although short-run deviations from the LOP may exist, long-run forces in the market ensure convergence in purchasing power parity across economies (Taylor & Taylor, 2004).

This mechanism restores domestic prices and the exchange rate toward the parity implied by PPP. Conversely, when the opposite occurs, the currency appreciates, and inflationary pressures emerge. Hence, the fundamental proposition of the PPP hypothesis is that, despite deviations from the Law of One Price, long-run market forces drive the equalization of purchasing power across nations (Taylor & Taylor, 2004).

2.2. Absolute and Relative PPP

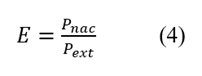

There are two standard versions of PPP: absolute (strong) and relative (weak). The absolute hypothesis, grounded in the LOP, holds that the exchange rate should equal the proportion of price levels between countries, assuming no distortions from government restrictions or transport expenses. As noted by Dornbusch (1993), both transportation costs and time operate as natural impediments to trade. This hypothesis holds when NER equalizes a currency’s purchasing power at home and abroad after conversion (Isard, 1995):

In terms of our approach:

![]()

The equation employs ![]() to denote NER,

expressed as units of foreign currency per one unit of local currency. Here,

to denote NER,

expressed as units of foreign currency per one unit of local currency. Here, ![]() corresponds to the

internal price level, and

corresponds to the

internal price level, and ![]() represents the

foreign price level.

represents the

foreign price level.

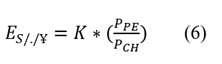

The relative version of PPP, however, relaxes the rigid assumptions of the absolute hypothesis by incorporating a constant factor “K”, symbolizing natural frictions and policy-induced trade barriers that allow for differences between exchange rates and relative prices.

Either variant implies a constant real exchange rate "Q":

![]()

If we apply logarithms to both sides of equation (7):

![]()

Given that “K” is constant, its log transforms to zero. Accordingly, the real exchange rate (Q) in logarithmic form must also remain constant, though not obligatorily at zero. Using lowercase letters for logarithms, the expression becomes:

![]()

According to both the absolute and relative formulations of PPP, fluctuations in the domestic-to-foreign price level ratio induce proportional variations in NER, which can be represented as:

![]()

Equation (10) indicates that movements in NER, expressed in percentage terms, are driven by the difference in inflation rates of Peru and China. Thus, the speed at which the currency gains or loses value corresponds directly to the inflation disparity between the countries.

Absolute PPP is constrained by the difficulty of constructing equivalent baskets of goods for meaningful international comparisons of purchasing power. Hence, empirical studies commonly employ the relative PPP framework, which maintains that exchange rate variations during a specific period correspond to cross-country differences in inflation rates. Importantly, while absolute PPP ensures the validity of relative PPP, the reverse is not guaranteed. According to Laurente Blanco & Machaca Hancco (2020), the hypothesis can be examined through extended models that, beyond domestic and international price levels, account for the tradable–non-tradable distinction or include productivity effects.

From a theoretical standpoint, departures from PPP should be corrected instantly through adjustments in domestic prices and exchange rates, thereby restoring equilibrium. In practice, however, trade barriers hinder this process, meaning PPP is not perfectly observed. Research findings reveal that departures from parity are generally short-lived, with prices adjusting toward convergence over time. This suggests that the real exchange rate must be a stationary process, without unit root properties. Hence, following an external shock—be it a fluctuation in prices or in NER—the series should return to its long-run mean. The present study tests this assumption using the econometric approach advanced by Rogoff (1996):

![]()

3. ECONOMETRIC MODEL

3.1. Data description

For empirical analysis, data were drawn from the records of the BCRP and the IMF. The dataset covers 228 monthly observations between 2002 and 2019, serving as the foundation for evaluating the evolution of exchange rates and inflation rates in the Peruvian and Chinese economies.

3.2. Model description

In this research, the hypothetical-deductive method is used, since it starts from the observation of a fact, in this case, the current trade relationship between Peru and China. Then, a hypothesis is proposed, which is corroborated through econometric tests, which allow us to contrast if what the theory dictates coincides with reality. In this study, the population corresponds to the collection of possible monthly realizations of changes in the PEN/CNY nominal exchange rate, together with the inflation rates of both Peru and China. The sample is made up of statistical data from 2002 to 2019 (eighteen years), analyzed monthly, with which the sample universe is 216 data.

Likewise, a non-experimental research design was developed, because the variables were not modified or manipulated; they were studied in their natural context. It was also longitudinal, as the variables were analyzed over a determined period, from 2002 to 2019.

Table 1

Operationalization of Research Variables

|

Variable |

Conceptual definition |

Operational definition |

Indicator |

Instrument |

|

NOMINAL EXCHANGE RATE |

It is the price at which one currency is negotiated relative to another. If the national currency is sol, then it is interpreted be the number of soles needed to buy one Chinese yuan. |

Monthly exchange rate information for the PEN and the CNY from 2002 to 2019. |

Bilateral index |

BCRP statistical data |

|

INFLATION IN PERU |

It is the generalized increase in prices in an economy that resulting in a decline in the purchasing power of its currency. |

Monthly data on Peru's inflation rate from 2002 to 2019. |

Index (2010 base=100) |

IMF Statistics |

|

CHINA INFLATION |

It is the persistent increase in prices, in this case, of the Chinese economy, which results in the loss of the purchasing value of the currency. |

Monthly year-on-year changes in China's CPI from 2002 to 2019. |

Index (2010 base=100) |

IMF Statistics |

3.3.Data collection techniques and instruments

The present research relied on 216 historical data points that were arranged, categorized, and processed using statistical software tools. Data collection techniques included the extraction of statistical information from sources such as the BCRP and the IMF, as well as consulting bibliographic backgrounds, research articles, and specialized documents. The analysis was conducted using econometric software such as R-Studio 4.0.2 and Eviews 10, which were also used as tools for data processing

3.4.Methodological strategies

To test the hypothesis, the first step was to evaluate whether each of the variables had a unit root, which allows analyzing their degree of stationarity. The analysis employed unit root tests such as ADF, PP, and ERS. Based on these, a VECM was estimated to determine the optimal lag structure and evaluate variable exogeneity. This framework enabled the study of both long-run cointegration and short-run adjustments. Additionally, robustness was verified through diagnostic procedures that tested residual normality, heteroskedasticity, and autocorrelation.

The methodological approach described is consistent with previous studies that have evaluated PPP in various economies. or example, Xie et al. (2021) applied a similar methodology in their analysis of PPP in developed and emerging economies, emphasizing the importance of assessing stationarity and long-term relationships among key variables.

Kamran Khan et al. (2019) also utilized ADF and PP tests to examine whether the USD/CNY exchange rate is cointegrated with several macroeconomic indicators. The results demonstrated evidence of a long-term equilibrium, thereby supporting the methodological soundness of this approach in the study of exchange rates within integrated economies.

In their study on PPP involving Pakistan, Iran, Turkey, and China, She et al. (2020) employed Johansen’s cointegration test and a VECM to examine long-term interactions between exchange rates and inflation. The evidence confirmed the validity of PPP in the long run, while short-run discrepancies were attributed to factors like trade barriers and transaction costs. These observations highlight the relevance of this methodological approach in analyzing PPP between Peru and China, where structural differences between the two economies could explain the dynamic behavior of exchange rates and inflation rates.

3.4.1. Regression Model Specification

In the proposed regression framework, the dependent variable is the yearly change in the PEN/CNY nominal exchange rate, which captures the response of the exchange rate to the bilateral economic conditions. The key explanatory variable is the inflation differential, obtained by subtracting China’s inflation from Peru’s. The model aims to assess the impact of inflation disparities on exchange rate fluctuations, consistent with Edwards (2006), who underscores the connection between inflation differentials and nominal exchange rate dynamics.

The proposed econometric formulation is as follows:

![]()

Where![]() represents the

year-over-year fluctuation in the nominal PEN/CNY exchange rate. Additionally,

represents the

year-over-year fluctuation in the nominal PEN/CNY exchange rate. Additionally, ![]() denotes the

inflation rate in Peru, while

denotes the

inflation rate in Peru, while ![]() indicates the inflation

rate in China. Finally,

indicates the inflation

rate in China. Finally, ![]() refers to the residual

expression, which captures the unexplained variability in the model.

refers to the residual

expression, which captures the unexplained variability in the model.

In this specification, β is anticipated to take the value of one. Accordingly, a one-percent rise in Peru’s inflation compared to China’s would generate a one-percent depreciation of the PEN, with the opposite effect occurring if the differential decreases. This outcome reflects the conditions required for relative PPP to hold.

The assumptions established for the regression model are as follows: First, it is assumed that Peru and China present different levels of economic development, considering Peru as a developing country and China as a developed economy. Another assumption is price homogeneity, whereby price variations translate proportionally into movements of NER. Additionally, the long-run validity of PPP is imposed, implying that the model’s parameters must meet the restrictions α = 0 and β = 1. Such assumptions are critical for the proper interpretation of outcomes and for maintaining the robustness of the conclusions.

4. RESULTS AND DISCUSSION

4.1.1. Evolution of Peru's inflation rate

The behavior of inflation in Peru throughout the study period was initially unstable, as shown in Figure 1. This reflects the residual effects of an inflationary and political crisis experienced by the country in previous decades. Starting in 2002, the BCRP implemented an Explicit Inflation Targeting scheme, setting a target range between 1% and 3% to anchor the expectations of economic agents and promote price stability (BCRP, 2019). During the period 2002-2009, inflation in Peru was relatively low and stable, with an annual average of 2.6%. However, inflationary peaks were recorded at certain key moments (BCRP, 2014). For example, in 2004, prices rose due to an overall increase in the cost of fuel, urban transport, and food products like wheat and soybeans, which affected the cost of basic goods in the country. Additionally, a severe drought that year reduced agricultural production, impacting important crops such as rice and sugar. The year 2008 marked the highest point of inflation in Peru during the study period, driven mainly by the increase in global commodity prices as a result of the financial crisis. Inflation reached levels not seen since the 1970s, with significant increases in the price of essential foods like wheat, corn, and soybeans (Salas, 2009). However, by the end of 2009, inflation rates fell considerably thanks to the recovery of international markets and corrective measures implemented by the BCRP.

In the following years, inflation in Peru remained relatively controlled, although some external and climatic events caused temporary fluctuations. For example, the La Niña phenomenon in 2011 seriously affected agricultural and livestock production, generating water shortages. In 2015, a higher exchange rate in 2015 affected the price level, while in 2017, the El Niño phenomenon had a strong impact on agricultural products, again influencing inflation.

4.1.2. China's inflation rate evolution

In contrast, the evolution of inflation in China during the same period was much more volatile, as shown in Figure 1. In the early years of the study, between 2002 and 2004, China maintained relatively low levels of inflation. The IMF (2021) notes that domestic reforms and trade liberalization played a key role in sustaining price control, particularly after China joined the WTO in 2001, which boosted international trade. At the same time, the privatization of state enterprises further supported price stability. Despite prior reforms, the Chinese economy was strongly affected by the 2008 global financial crisis. To counteract its effects, authorities implemented expansionary policies—such as increased government spending and lower taxes—resulting in a significant inflationary uptick (Fang et al., 2009). Food prices, especially commodities like pork, increased due to climatic problems and rising agricultural production costs (Sornoza Parrales et al., 2018).

Starting in 2009, China experienced a phase of deflation, driven by price control policies and a decrease in tariffs on imports of raw materials, which led to a drop in global prices. However, this trend was reversed in 2011, when rains and floods affected agricultural production and caused an increase in food costs, leading to a new inflationary wave (Fan, Kanbur, & Zhang, 2010). In the following years, inflation rates in China were more controlled thanks to a series of restrictive monetary policies implemented by the government, although the risk of deflation was a concern towards the end of the study period. Despite the moderation in inflation, the government's expansionary policies and China's rapid economic growth continued to put pressure on domestic prices.

Figure 1

Evolution of Inflation in Peru and China

4.1.3. Evolution of NER PEN/CNY

A relatively stable trend in NER of PEN/CNY was observed over the period from 2002 to 2019, as shown in Figure 2. This behavior is attributed to various internal and external factors that influenced the evolution of the exchange rate over the years.

In 2002, the PEN was one of the currencies that depreciated the least in Latin America, with a real appreciation of 0.6%. This result occurred within the context of macroeconomic stability and inflation control by BCRP, which implemented measures to mitigate domestic inflationary pressures, as reported by BCRP (2002). In 2003, however, NER showed a slight depreciation, driven mainly by the increase in inflation due to variations in external prices, specifically the appreciation of the US dollar, which was Peru's main trading partner at the time, according to BCRP (2004).

NER registered a slight decrease at the close of 2004, primarily reflecting PEN appreciation during the second semester. According to BCRP (2005), this behavior was supported by a trade balance surplus and higher remittance inflows, which increased the demand for the local currency.

Between 2006 and 2007, NER rose slightly due to lower inflation in Peru compared to its trading partners. This increase was moderate, as the Peruvian economy showed signs of stability (BCRP, 2007). Nevertheless, amid the 2008–2009 global financial crisis, NER experienced a pronounced increase of nearly 16.7% compared to the previous year, reaching a peak of 0.47 PEN/CNY in February 2009, a consequence of global economic volatility that affected emerging economies, including Peru, as highlighted by Claessens, Ayhan Kose, and Terrones (2010).

Towards the end of 2009 and the beginning of 2010, the exchange rate began to stabilize. The measures adopted by the BCRP and the gradual recovery of international markets contributed to keeping the exchange rate at more controlled levels, which allowed it to remain stable until 2015 and 2016, according to BCRP (2010).

In 2015, the PEN depreciated again, largely due to the high volatility of international financial markets and the fall in prices of Peru's main export commodities, such as copper and gold. This depreciation reflected growing global uncertainty and declining demand for commodities from emerging economies, including China, as noted by BBVA Research (2016).

Finally, at the end of 2016, the PEN showed significant appreciation, driven by the recovery in commodity prices and Peru's strong economic performance. Additionally, lower uncertainty regarding China’s economic growth contributed to this appreciation, due to the stability of the trade market with its main Asian partner. In the following years, NER between PEN/CNY remained relatively stable, reflecting greater stability in international markets and in the monetary policies implemented by both countries, as reported by BBVA Research (2017).

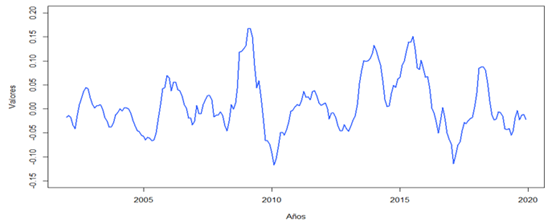

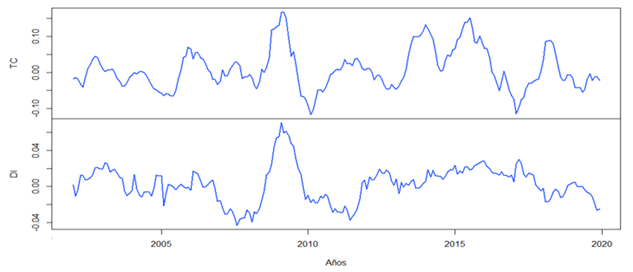

Figure 3 shows the Exchange Rate Variation (ER) and the difference in inflation rates (ID) share a parallel trend between the Peruvian and Chinese economies, which verifies that relative parity is present. In addition, the evolution of these series seems to be non-stationary, both in mean and variance.

Year-on-year change in NER PEN/CNY

Exchange Rate Variation vs Inflation Rate Difference

4.1.4. Descriptive statistics of the variables

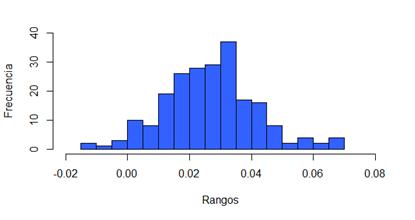

During the period under analysis, Peru’s inflation rates fluctuated notably, ranging between -1.11% and 6.78%, as depicted in the histogram in Figure 4.The average was 2.73%, which is within the inflation target range set by the BCRP. The kurtosis value of 3.37 indicates that extreme values are more prevalent than those found in a standard normal distribution. However, the asymmetry of 0.215, close to zero, indicates that the series does not show significant bias towards either end of the distribution. Additionally, with a p-value of 0.171, the normality test suggests that the null hypothesis of normal distribution is not rejected at the 5% significance threshold. These results allow us to conclude that inflation in Peru during the period analyzed follows a normal distribution, an important indicator to validate the necessary assumptions in the econometric analysis and exchange rate modeling under the PPP theory.

However, as they point out by Xie et al. (2021), structural changes in the economy can affect the validity of PPP theory, especially when considering open economies such as Peru and China. According to his analysis, the presence of permanent or temporary breaks in the exchange rate can generate significant deviations in the short term, which highlights the importance of evaluating not only the normality of the inflationary series, but also the possibility of abrupt or gradual changes in the underlying economic dynamics.

Histogram of Inflation Frequencies of Peru (2002-2019)

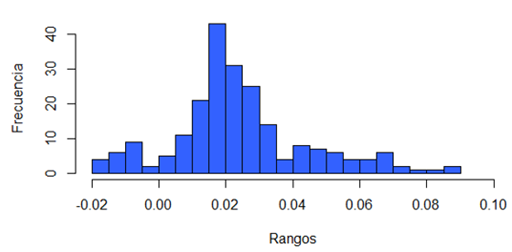

Inflation in China presented a wide variability, fluctuating between a minimum of -1.79% and a maximum of 8.8%. Kurtosis of 3.84 indicates a greater presence of extreme values compared to a normal distribution. On the other hand, the asymmetry of 0.67 shows a positive bias, i.e., the distribution is tilted towards higher values, implying that China's inflationary behavior in this period was influenced by some significant inflationary peaks. The Jarque-Bera test indicates a 22.9% probability, supporting the acceptance of inflation’s normal distribution assumption. Although the results show certain deviations from the normal distribution as can be seen in Figure 5, such as positive asymmetry and high kurtosis, the normality test suggests that, at an acceptable confidence level, the series follows an approximately normal behavior, which supports the validity of its inclusion in the econometric model to assess PPP in the relationship between Peru and China.

Figure 5

China's Inflation Frequency Histogram (2002-2019)

4.1.5. Unit root test

Unit root analysis of the TC series reveals non-stationarity in levels, which is corrected by first differencing (Table 2). This confirms the series is I(1). The finding aligns with the hypothesis that nominal exchange rates in open economies usually follow a random walk, making differences necessary for stationarity.

For the inflation differential (DI), ADF and ERS tests show non-stationarity at 5%, and PP at 1%, but first differencing achieves stationarity in most tests, indicating I(1) integration. This is key for PPP, which posits long-term cointegration between inflation differentials and exchange rates.

Finally, the results confirm the first condition necessary for validating the PPP: the existence of integrated series of order one. Consequently, a cointegration framework can be employed to assess the presence of a long-term equilibrium relationship between the series, a key step in confirming or rejecting the PPP hypothesis within the analyzed context.

Table 2

Unit Root Test

|

|

With Intercept and without Trend |

|

With Intercept and Trend |

||

|

|

Level |

First Difference |

|

Level |

First Difference |

|

Exchange rate (TC) |

|

|

|

|

|

|

Dickey-Fuller Augmented (BIC) |

Non-stationary |

Stationary |

|

Non-stationary |

Stationary |

|

Elliot, Rothenberg and Stock (P-test) |

Non-stationary |

Stationary** |

|

Non-stationary |

Stationary** |

|

Phillips-Perron |

Non-Stationary* |

Stationary |

|

Non-stationary |

Stationary |

|

Inflation Difference (DI) |

|

|

|

|

|

|

Augmented Dickey-Fuller Test (BIC) |

Non-stationary |

Stationary |

|

Non-stationary |

Stationary |

|

Elliot, Rothenberg and Stock |

Non-stationary |

Non-stationary |

Non-stationary |

Non-stationary |

|

|

Phillips-Perron |

Non-Stationary* |

Stationary |

|

Non-Stationary* |

Stationary |

*At 1% significance, at 5% it is stationary

**DF-GLS

4.1.6. Cointegration Test

Relative PPP for Peru and China was assessed by investigating the long-term relationship between nominal exchange rate changes and inflation differentials, using Johansen and Phillips-Ouliaris cointegration methods.

As shown in Table 3, the Johansen test identifies a cointegration vector at the 5% significance threshold for both the trace and maximum eigenvalue tests, with an optimal lag length of fifty-seven. It should be noted that, in similar studies, such as that of She, Zakaria, Khan, and Jun (2020), a result like the one obtained in the trace test (statistic of 25.55 vs. a critical value of 19.96) is considered robust and falls within the expected range for studies with long time series. This indicates that the long-term relationship is robust, even in complex economic contexts such as Peru and China. Similarly, the Phillips and Ouliaris test confirms cointegration, with a t-statistic of 82.4094, which nearly doubles the critical value of 40.8217, interpreted as a strong signal of cointegration, well above what is typically found in studies analyzing currencies with more stable dynamics.

The analysis confirms a partial validation of PPP in the Peru–China trade context from 2002 to 2019. Inflation differentials between the two countries, alongside external events and structural factors, significantly influence the exchange rate, such variations are driven by both inflationary gaps and external shocks, including the 2008 financial crisis and weather-related events like El Niño and La Niña. These external shocks had substantial impacts on both economies, with Peru—due to its heavy reliance on raw material exports—showing greater vulnerability and experiencing pronounced effects on its purchasing power, China’s diversified economy mitigated short-term exchange rate impacts on prices, and cointegration between inflation and NER points to long-term equilibrium, in line with PPP theory; however, the magnitude and speed of this adjustment are influenced by structural factors not fully captured in the model, suggesting that additional variables or constraints could enhance our understanding of exchange rate behaviour. For instance, the application of fractional integration techniques, as seen in studies by Gil Alana and Jiang (2011), could offer a more detailed perspective on the persistence and long-term mean reversion in exchange rate dynamics, underscoring the complexity of achieving complete PPP validation in emerging markets.

Table 3

Cointegration analysis results

|

Johansen Cointegration Test |

Trace Statistician |

Critical Value (5%) |

Statistician Max Eigen |

Critical Value (5%) |

|

None |

25.55 |

19.96 |

16.77 |

15.67 |

|

At most 1 |

8.78 |

9.24 |

8.78 |

9.24 |

|

Phillips and Ouliaris test |

T Statistic |

Critical Value (5%) |

||

|

There is co-integration |

82.4094 |

40.8217 |

||

4.2.Regression model

4.2.1. Error Correction Vector Model

Using a VECM approach, the analysis detected cointegration between inflation and NER, suggesting convergence toward long-run equilibrium even if short-run adjustments were incomplete. Subsequently, a VECM was employed to capture both the long-term linkage and the short-term responses of nominal exchange rate changes to inflation disparities between Peru and China. With 216 monthly observations (January 2002 - December 2019), the model specifies a lag of 9 periods for the DI variable (inflation difference), which reflects that the impact of inflationary differences is not immediate but propagates over time. As equation (12) shows, the estimated coefficient for the inflation difference is 0.8307, which indicates that an increase of one unit in the inflation difference causes an increase of 0.83 in the variation of NER in the short term. This result is consistent with the theory of relative PPP, which suggests that higher inflation in a country should lead to a proportional depreciation of its currency against that of its trading partner. In similar studies using VECM models, the coefficients for the inflationary difference are usually in a range close to 1, so this result is within expectations. In addition, this value reinforces the hypothesis that the PPP is partially fulfilled in the long term in the relationship between Peru and China, given that a correction mechanism is observed that adjusts short-term deviations towards a long-term equilibrium. The slightly lower ratio may be due to structural factors such as trade barriers, divergent monetary policies, or foreign exchange market rigidities, which limit full adjustment.

Bahmani-Oskooee (1998) analyzes how devaluations in developing countries are often influenced by structural factors, causing exchange rate adjustments to be neither immediate nor complete due to these constraints. Similarly, other studies have found consistent results when analyzing pairs of economies with asymmetric development levels, such as Thailand or Iran, where strong relationships are also identified between inflation differences and exchange rate variations, but with coefficients that do not reach full unity, indicating that short-term adjustments are imperfect. Therefore, the results of this model align with theoretical expectations and prior empirical studies, supporting the validity of the PPP hypothesis in the case of Peru and China.

D(TC)=0.00181228+0.830727667D(DI) (12)

To verify whether the estimated coefficients are statistically equivalent to -1 and 0, a constraint test was performed in the cointegration model, proposing the following null hypotheses:

B(1,2)=−1B(1,2) = -1B(1,2)=−1 and A(1,1)=0A(1,1) = 0A(1,1)=0

The likelihood ratio statistic obtained is 9.6, with an associated probability of 0.0082. Since this probability is less than the 5% significance level, the null hypothesis is rejected. This implies that the estimated coefficients, -0.8037 and -0.0001, are not equal to -1 and 0, respectively.

From a PPP validation perspective, this result suggests that even though a long-run relationship exists between the variables, the fit is not perfect. In particular, the coefficient -0.8037, although close to -1, suggests that the impact of inflationary differences on the exchange rate is not completely proportional, which could be related to structural factors in the economies of Peru and China, such as exchange rate policies or trade barriers that prevent full adjustment. Also, the coefficient close to 0 (-0.0001) indicates that there is an error correction in the system, but with a limited adjustment speed.

Similar studies evaluating PPP found that although the long-term relationship is statistically significant, the coefficients often deviate from theoretical values due to factors such as market frictions and differences in inflationary dynamics. Therefore, the results of this test are consistent with theoretical expectations and with previous empirical evidence.

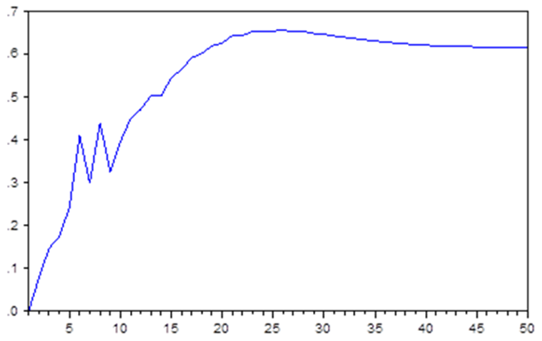

Figure 6 illustrates the speed of error adjustment. The analysis of the impulse-response function indicates that after a one-standard deviation shock to the inflation differential causes NER to increase for approximately 24 months before stabilizing. This trend indicates that, although the initial impact is significant, the system gradually corrects deviations toward long-run equilibrium, supporting the existence of a stable relationship between the variables. This finding is consistent with Holmes (2001), who finds that adjustment time is slightly faster in developing countries compared to industrialized countries, though convergence towards PPP remains slow. Regarding the long-run relationship, the equation obtained is:

TC= 0.8037 * DI

This implies that a one-percentage point increase in the inflation differential (Peru-China) results in an approximate 0.80 percentage point depreciation of the Peruvian currency, with a 90% confidence level. However, the coefficient being less than 1 suggests an incomplete pass-through, indicating that relative PPP is not perfectly fulfilled. This result is common in emerging economies, where factors like exchange controls and market rigidities affect the complete adjustment predicted by the theory.

Similar results have been found in previous studies. For example, the research conducted by She et al. (2020) on the relationship between emerging economies shows that PPP tends to be partially fulfilled, with coefficients oscillating around values less than 1, suggesting that other factors influence exchange rate determination.

Impulse response function

5. CONCLUSIONS

This study analyzed the validity of the PPP theory in its relative form between Peru and China over the period 2002-2019. The results demonstrate a partial fulfilment of the theory, revealing that inflation differentials between the two economies influence NER, though the effect is not entirely proportional. This partial compliance suggests that, while PPP offers a valuable framework for comprehending long-term exchange rate movements, its predictions are moderated by various structural and external factors, particularly in emerging market contexts like Peru.

One key finding is that exchange rate dynamics are shaped by a combination of inflationary disparities and significant external events. For instance, periods of heightened economic uncertainty, such as the 2008 global financial crisis, along with climate phenomena like El Niño and La Niña, introduced volatility that impacted Peru more acutely due to its reliance on raw material exports. Such events underscore the importance of recognizing economic structure when assessing Purchasing Power Parity applicability, as economies dependent on commodity exports may experience fluctuations in purchasing power and competitiveness when their currencies appreciate. In contrast, China’s more diversified economic base provides greater resilience to such shocks, helping to mitigate the direct effects of exchange rate variations on its domestic purchasing power.

The econometric analysis using a Vector Error Correction Model identified a cointegration relationship between inflation rates and NER, suggesting that both variables exhibit a tendency to converge towards a long-term equilibrium. However, the incomplete nature of the short-term adjustments indicating that PPP theory does not fully capture the complex dynamics of the exchange rate in the short run. This finding holds particularly relevant for policymakers, as it highlights the limited ability of inflationary differences alone to predict immediate exchange rate movements and suggests that additional variables, such as structural economic factors and global macroeconomic conditions, play a crucial role.

From a policy perspective, these results have important implications for Peru. Policymakers should account not only for domestic inflation trends but also for the macroeconomic developments in China, which, as Peru's main trading partner, has a significant impact on both countries' trade and exchange rate stability. Ensuring stability in the exchange rate and mitigating vulnerability to external shocks should be prioritized to foster sustainable economic growth and protect purchasing power. Furthermore, this research highlights the potential value of foreign exchange market interventions and strategic adjustments in trade policies to offset the impacts of sudden economic shifts, helping to maintain economic stability in an increasingly interconnected global economy.

In conclusion, while PPP theory provides a meaningful basis for examining long-term trends, this study’s findings underscore the need to consider country-specific characteristics, economic structure, and external pressures when applying PPP in diverse economic contexts. Future research may explore the inclusion of additional variables, such as Gross Domestic Product and interest rates, to develop a more comprehensive understanding of the inflation-exchange rate relationship and support the formulation of more effective economic policies in the context of Peru-China relations.

Bahmani-Oskooee, M. (1998). Are Devaluations Contractionary in LDCs? Journal of Economic Development, 23(1):131-145.

Bawono, S. (2019). Dynamics Of Real Exchange Rate and Three Financial Crisis: Purchasing Power Parity Relative Approach In Indonesia And Thailand. International Journal of Scientific & Technology Research.

BBVA Research. (2016). Peru | Where is the exchange rate headed? Retrieved from https://www.bbvaresearch.com/wp-content/uploads/2016/11/Observatorio-tipo-de-cambio-final-1.pdf

BBVA Research. (2017). Peru Situation.

BCRP. (2002). Annual Report.

BCRP. (2004). Inflation Report.

BCRP. (2005). Inflation Report.

BCRP. (2007). Annual Report.

BCRP. (2010). Annual Report.

BCRP. (2014). Inflation targeting and Quantitative Tightening: Effects of Reserve Requirements in Peru. Central Reserve Bank of Peru. Retrieved from https://www.bcrp.gob.pe/docs/Publicaciones/Documentos-de-Trabajo/2014/documento-de-trabajo-03-2014.pdf

BCRP. (2019). Inflation Report: Current Outlook and Macroeconomic Projections.

BCRP. (2020). Annual Report.

Claessens, S., Ayhan Kose, M., & Terrones, M. (2010). The global financial crisis: How similar? How different? How costly? Asian Economic Policy Review. https://doi.org/10.1016/j.asieco.2010.02.002

Comex Peru. (2020). PERU-CHINA FTA: A DECADE OF GAINS. Retrieved from https://www.comexperu.org.pe/articulo/tlc-peru-china-una-decada-de-ganancias

Craig, B. (2005). The Growing Significance of Purchasing Power Parity. Federal Reserve Bank of Cleveland. Retrieved from

https://www.clevelandfed.org/publications/economic-commentary/2005/ec-20050401-the-growing-significance-of-purchasing-power-parity

Edwards, S. (2006). The Relationship Between Exchange Rates and Inflation Targeting Revisited. National Bureau of Economic Research (NBER).

https://doi.org/10.3386/w12163

Fan, S., Kanbur, R., & Zhang, X. (2010). China's regional disparities: Experience and policy. Review of Development Finance, 1(1):47-56.

https://doi.org/10.1016/j.rdf.2010.10.001

Fang, C., Yang, D., & Meiyan, W. (2009). Crisis or Opportunities: China's Response to the Global Financial Crisis. The perspective of the world review, 1(1):91-113.

Gil Alana, L., & Jiang, L. (2011). The Purchasing Power Parity Hypothesis in the US–China Relationship: Fractional Integration, Time Variation and Data Frequency. International Journal of Finance & Economics, 18(1):82-92. https://doi.org/10.1002/IJFE.461

H. Cordesman, A. (2023). China's Emergence as a Superpower. Center for Strategic and International Studies (CSIS). Retrieved from https://www.csis.org/analysis/chinas-emergence-superpower

Holmes, M. (2001). New Evidence on Real Exchange Rate Stationary and Purchasing Power Parity in Less Developed Countries. Journal of Macroeconomics, 23(4):601-614. https://doi.org/10.1016/s0164-0704(01)00180-x

Imbz, J., Mumtaz, H., O. Ravn, M., & Rey, H. (2005). PPP Strikes Back: Aggregation and the Real Exchange Rate. Quarterly Journal of Economics, 120(1):1-43. https://doi.org/10.1162/0033553053327524

MFIs. (2021). People's Republic of China: 2020 Article IV Consultation-Press Release; Staff Report; and Statement by the Executive Director for the People's Republic of China.

Isard, P. (1995). Exchange Rate Economics.

Kamran Khan, M., Zhou Teng, J., & Imran Khan, M. (2019). Cointegration between Macroeconomic Factors and the Exchange Rate USD/CNY. Financial Innovation, 5(5). https://doi.org/10.1186/s40854-018-0117-x

Laurente Blanco, L. F., & Machaca Hancco, F. (2020). Econometric analysis of purchasing power parity in Peru. Ecos de Economía. 24(50), 4–24. https://doi.org/10.17230/ecos.2020.50.1

M. Taylor, A., & P. Taylor, M. (2004). The Purchasing Power Parity Debate. Journal of Economic Perspectives.

Murat Doğanlar, F. M. (2020). Testing the validity of purchasing power parity in alternative markets. Journal of International Financial Markets, Institutions and Money, 21(4):375-383. https://doi.org/10.1016/j.bir.2020.12.004

Nathaniel, O. O. (2019). Validity of Purchasing Power Parity (PPP) Hypothesis in the Ecowas (1980–2017). Emerging Economy Studies, 5(2), 141-156. https://doi.org/10.1177/2394901519870886

Phiri, A. (2017). Nonlinear adjustment effects in the purchasing power parity. Journal of Economics and Econometrics. 60(2):14-38

Rogoff, K. (1996). The Purchasing Power Parity Puzzle. Journal of Economic Literature, 34:647-668. https://doi.org/10.2307/2729217

Salas, J. (2009). What explains the fluctuations in inflation in Peru in the period 2002 – 2008? Evidence of a structural VAR analysis. BCRP. Estudios económicos, 16:9-36.

Salcedo Muñoz, V. (2020). Purchasing Power Parity (PPP) Theory: Gustav Cassel's contributions on the equilibrium exchange rate. Venezuelan Journal of Management (RVG). 25(92), 1837-1849. https://doi.org/10.37960/rvg.v25i92.34299

She, F., Zakaria, M., Khan, M., & Jun, W. (2020). Purchasing Power Parity in Pakistan: Evidence. Emerging Markets Finance and Trade, 57(13):3835-3854. https://doi.org/2019.1709820

Sornoza Parrales, G., Parrales Poveda, M., Sornoza Parrales, D., & Guaranda Sornoza, V. (2018). Economic reform of China: from planned economy to market economy. Revista Venezolana de Gerencia, 23(83), 521-529.

https://doi.org/10.37960/revista.v23i83.24261

Urriola Canchari, N., Osterloh Mejía, M., & Deng, X. (2020). The impact of Chinese Foreign Direct Investment on economic growth of Peru: a short and long run analysis. Latin American Journal of Trade Policy, 6:32-47.